Key Highlights

- On May 19, U.S. spot Bitcoin ETFs recorded net inflows of $667.4 million, marking the highest figure since May 2, driven by $306 million into the iShares Bitcoin Trust.

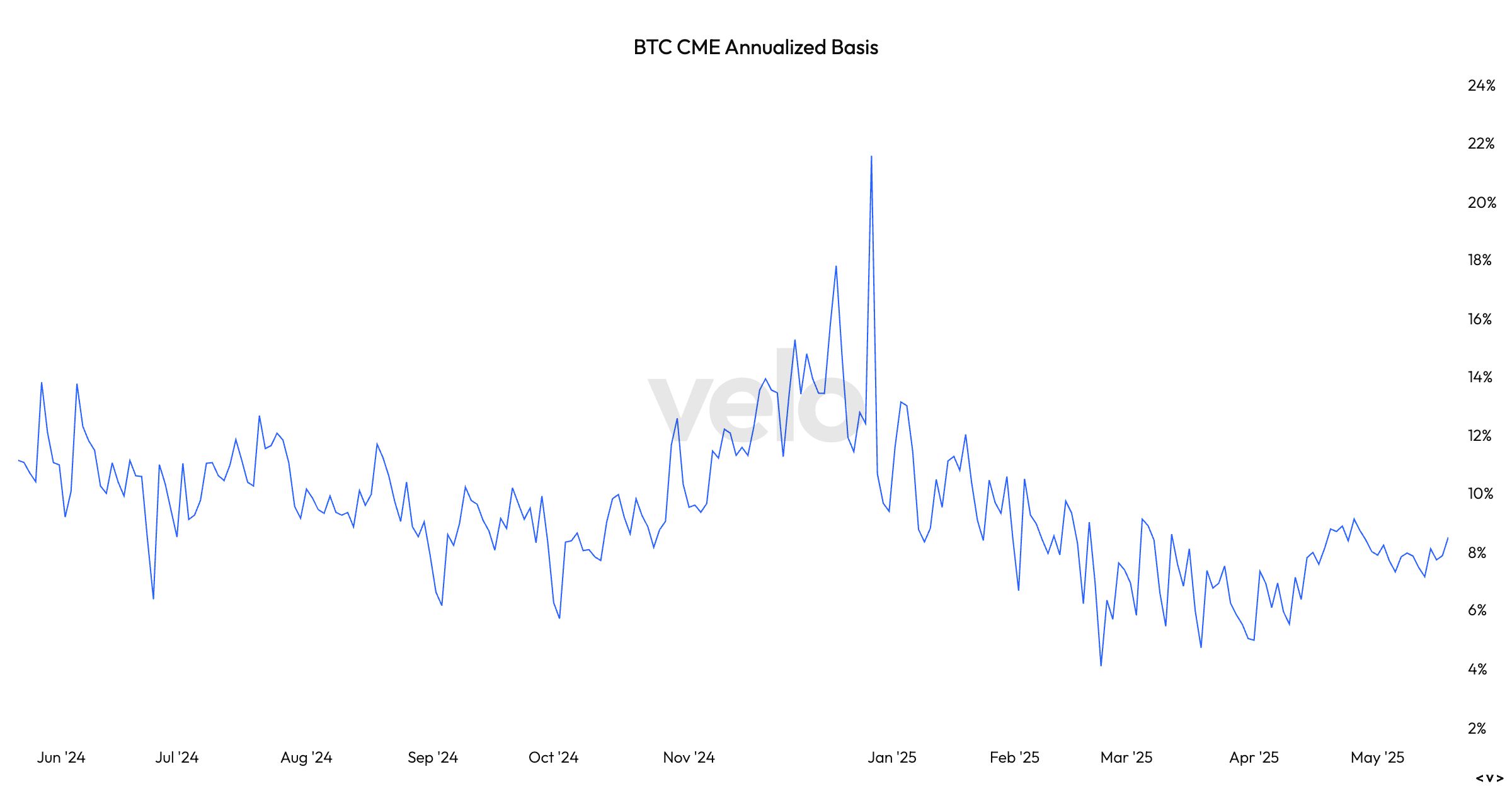

- Investor interest has surged as Bitcoin’s price holds steady above $100,000, coupled with a basis trade yield nearing 9%, leading to increased futures trading and institutional re-engagement.

Bitcoin Performance & Market Dynamics

The U.S.-listed spot Bitcoin exchange-traded funds (ETFs) recorded $667.4 million in net inflows on May 19, the highest in recent weeks, indicating renewed institutional interest. Nearly half of these inflows, amounting to $306 million, went into iShares Bitcoin Trust (IBIT), which has now reached $45.9 billion in total net inflows, according to data from Farside Investors.

This uptick in demand follows Bitcoin’s strong price performance, having traded above $100,000 for 11 consecutive days, restoring market confidence.

Furthermore, with the annualized basis trade becoming increasingly attractive, yields nearing 9% — almost double those observed in April — this strategy has gained traction, leading to increased trading activity in the CME futures market.

On that Monday alone, CME futures volumes surged to $8.4 billion (approximately 80,000 BTC), the highest volume since April 23. Meanwhile, open interest rose to 158,000 BTC, up over 30,000 BTC contracts from earlier lows, indicating growing interest in leveraged and arbitrage strategies.

Despite these increases, both futures volume and open interest remain significantly below the levels observed when Bitcoin peaked at an all-time high of $109,000 in January. This suggests potential for future growth.

Moreover, the increase in basis indicates that greater participation is occurring, welcoming back players who exited the market earlier this year when the basis fell to below 5%.

Recent disclosures also highlighted that the Wisconsin State Pension Board exited its ETF position in the first quarter, possibly in response to less favorable trading conditions. Given the lag in 13F filings and the subsequent widening of the basis spread from 5% to nearly 10%, it seems probable that they re-entered the market this quarter to capitalize on improved conditions.