Stablecoins Experience Unprecedented Growth in Q3 with $46 Billion Injection

Stablecoins have recorded their largest quarter ever, achieving an estimated net creation of $45.6 billion to $46 billion in Q3.

This represents a staggering 324% increase from Q2’s $10.8 billion, signaling a considerable influx of new capital into the market.

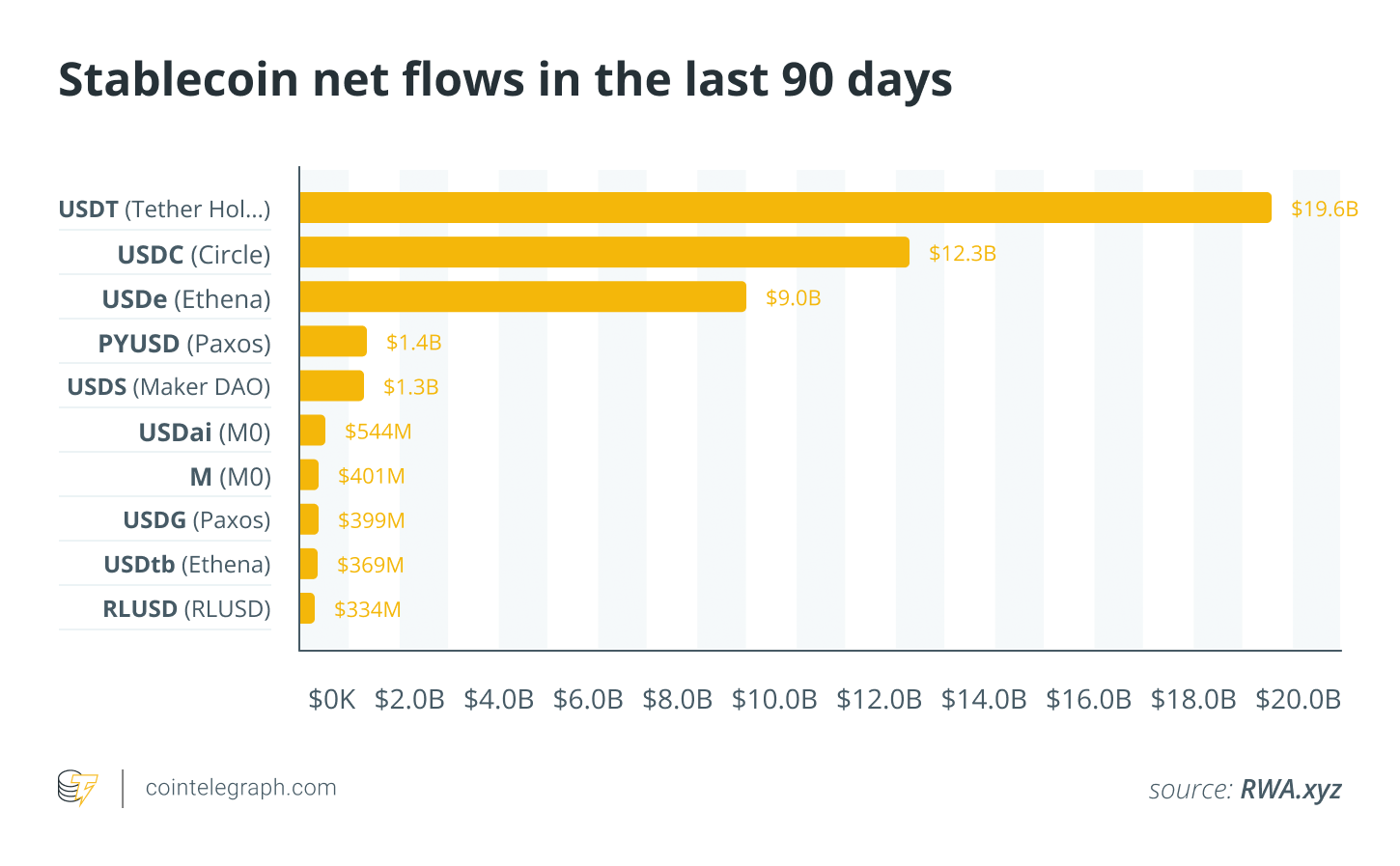

According to Cointelegraph, this remarkable surge was driven by various issuers: Tether’s USDt contributed about $19.6 billion, Circle’s USDC added approximately $12.3 billion, and Ethena’s USDe brought in around $9 billion. This mix combines established players with growing interest in innovative yield-bearing designs.

The current total for stablecoins stands within the $290 billion to $310 billion range. DefiLlama indicates nearly $300 billion in circulation, while recent calculations place it closer to $290 billion over the past month.

This trend showcases a larger, more liquid stablecoin market that enhances trading activities, supports decentralized finance (DeFi) collateral, and facilitates cross-exchange settlements.

Key Contributors to Growth

Most of Q3’s net expansion was concentrated among three major stablecoins:

- USDT: Dominating with $19.6 billion in net creations.

- USDC: Following with $12.3 billion, benefiting from wider distribution.

- USDe: Contributing $9 billion, catering to yield-sensitive investors despite ongoing discussions regarding risks and market conditions.

Beyond these three, emerging players like PayPal’s PYUSD and Sky’s USDS saw approximately $1.4 billion and $1.3 billion in quarterly inflows, respectively. Newer entrants, including Ripple’s RLUSD and Ethena’s USDtb, also posted modest but steady growth.

As we move forward into the next quarter, two primary queries arise: Can USDC continue to narrow the gap with USDT? And will USDe maintain its momentum amidst fluctuating market dynamics and regulatory considerations?

Where Capital is Concentrated

Most new funds have been allocated where liquidity is established:

- Ethereum holds over 50% of the total stablecoin supply (exceeding $150 billion).

- Tron follows with about $76 billion, favored for its low-fee transactions.

- Solana has positioned itself in third place, holding over $13 billion in native stablecoins due to expanding DeFi activity.

The distribution of capital reflects user preferences: Ethereum for composability, Tron for economical transfers, and Solana for efficient high-throughput usage.

Factors Behind the Stablecoin Resurgence

A combination of policy advancements, market dynamics, and technical improvements has paved the way for this growth:

- Policy clarity: The GENIUS Act has established the first US framework for payment stablecoins, promoting scalability among issuers.

- Yield attractiveness: High front-end rates and the rise of tokenized US Treasury bills have drawn in additional capital.

- Infrastructure improvements: Enhanced payment and exchange integrations, as well as faster and cost-effective L1/L2 solutions, have streamlined stablecoin operations.

- Risk management: Some of the surge can be attributed to investors sheltering funds in stablecoins amid volatile market conditions.

Winners and What Lies Beneath the Numbers

USDT and USDC captured the majority of new investments, bolstered by their exchange accessibility and extensive trading pairs.

Combined, they represent over 80% of the market. New regulations in the US further consolidate their positions. Ethena’s USDe also grew rapidly by emphasizing yield; however, it relies heavily on stable market conditions to maintain its stability.

Although PayPal’s PYUSD has gained traction due to enhanced distribution channels, Binance USD (BUSD) is gradually fading away, highlighting the importance of strategic partnerships.

That said, rapid growth does not equate to active utilization: in the past month, there has been a 23% decrease in active addresses and an 11% drop in transfer volumes. Much of the new supply appears more akin to cash reserves rather than active currency.

Liquidity remains thin across various platforms, leading to sharper price fluctuations during critical times. Emerging designs like USDe create additional demand but come with their own risks, having previously faced increased regulatory scrutiny.

The eye-catching figure of $46 billion signifies demand, but the pivotal matter is whether this supply converts into enduring activity, enhances liquidity, and endures future policy shifts or market pressures.

Future Trajectories to Monitor

Key indicators to observe as the market continues to develop:

- Creations vs. Redemptions: Is Q3’s $46 billion surge a fleeting event or the beginning of a new cycle?

- Issuer developments: Can USDC close the gap with USDT, and will USDe sustain growth without encountering stability issues?

- Blockchain conflicts: Watch how Ethereum, Tron, and Solana vie for market share, and whether emerging trends solidify.

- Infrastructure and ETFs: New SEC listing standards and products, such as CME’s SOL options, might stabilize market inflows.

- Policy implementation: Regulatory frameworks like the GENIUS Act and the EU’s MiCA will determine the future landscape for issuance and operational terms.

- On-chain dynamics: Innovations such as tokenized treasury bills alongside stablecoins could anchor liquidity balances.

Ultimately, the impressive statistic of $46 billion reflects significant interest, but the true challenge lies in maintaining this growth through sustained activity and resilience against potential regulatory changes or market disruptions.