$46 Billion Invested in Stablecoins Last Quarter: A Look at the Leaders

Stablecoins experienced a record influx of capital in Q3, with significant contributions from major players like Tether and Circle.

Stablecoins Making Headway

Stablecoins have just recorded their highest quarter yet, witnessing net creations estimated between $45.6 billion and $46.0 billion during Q3.

This marks a 324% increase compared to Q2’s $10.8 billion and signals a fresh influx of capital into the market.

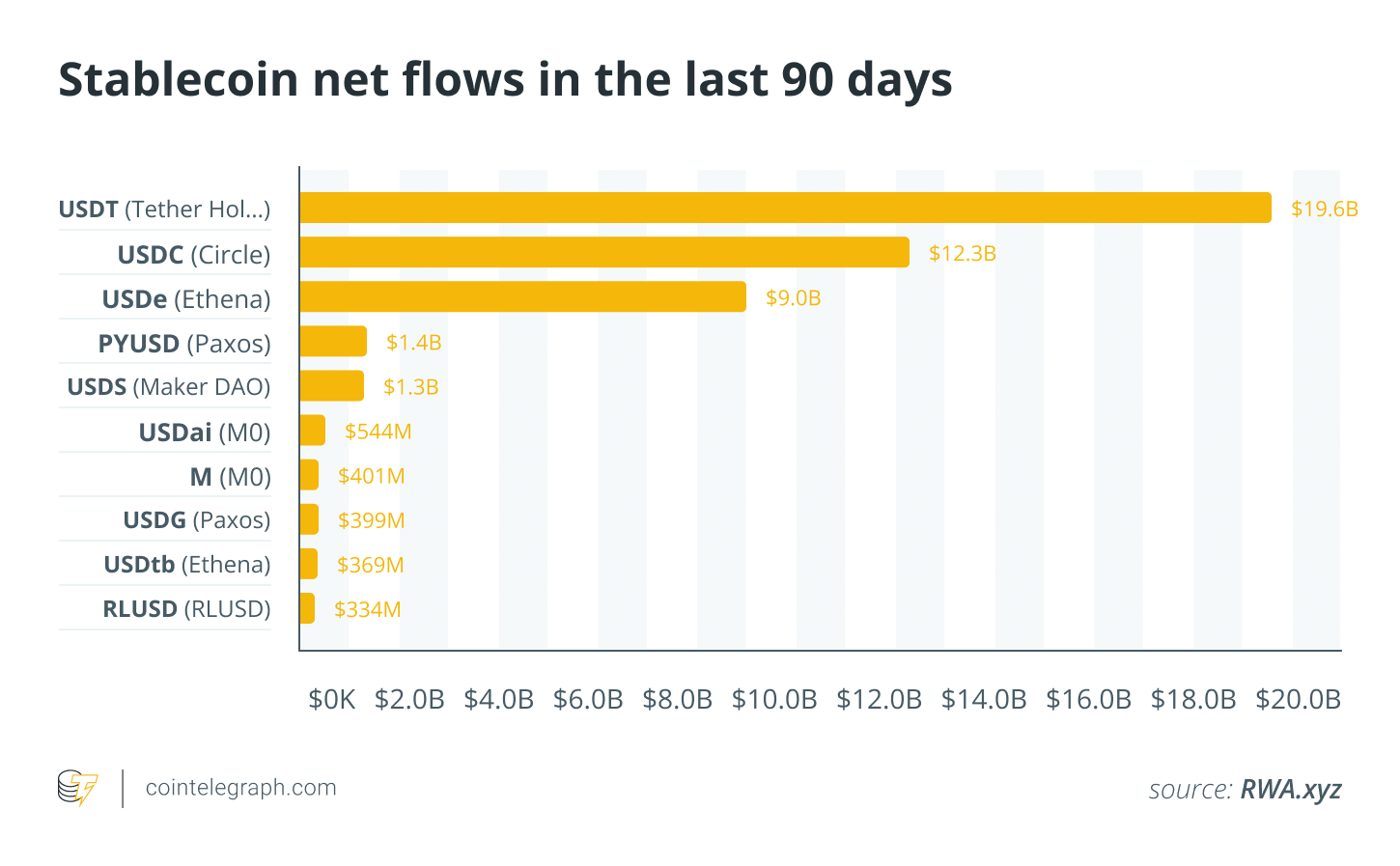

The surge was driven by several issuers: Tether’s USDt added approximately $19.6 billion, Circle’s USDC contributed around $12.3 billion, and Ethena’s USDe brought in about $9 billion. This blend highlights both established brands and growing interest in newer, yield-focused innovations.

Looking at the broader picture, the total stablecoin market cap fluctuates around the $290 billion-$310 billion range, with resources like DefiLlama indicating roughly $300 billion outstanding, while other industry metrics suggest a figure nearer to $290 billion over the past month.

The data underscores one core reality: a more substantial and liquid base of stablecoins enhances trading activities, bolsters DeFi collateral, and facilitates cross-exchange settlements.

Highlights from Q3

Most of the gains were concentrated among three main stablecoins:

- USDT: Dominated with $19.6 billion in new creations, solidifying its control over centralized exchanges and layer-1 (L1) and layer-2 (L2) networks.

- USDC: Followed with $12.3 billion, benefitting from improved accessibility and wider distribution.

- USDe: Contributed $9 billion, reflecting the appetite for yield-linked models amid ongoing market discussions concerning risks and structures.

Beyond these top three, PayPal’s USD (PYUSD) and Sky’s USDS saw inflows of roughly $1.4 billion and $1.3 billion, respectively. Newer players like Ripple’s RLUSD and Ethena’s USDtb also experienced moderate gains from a lower initial base.

Looking ahead, two critical questions loom: will USDC close the gap with USDT, and can USDe maintain its growth trajectory as market dynamics shift and regulatory changes impact operations?

Factors Behind the Stablecoin Revival

A combination of policy adjustments, market trends, and technological upgrades has paved the way for renewed interest:

- Policy Clarity: The GENIUS Act provides a foundational framework for payment stablecoins in the U.S., boosting issuer confidence.

- Yield Opportunities: Rising rates and tokenized U.S. Treasurys — which jumped from about $4 billion to over $7 billion — attracted further investment.

- Infrastructure Improvements: Enhanced payment and exchange integrations have simplified stablecoin usage since the previous year.

- Investor Strategies: Increased capital inflow reflects cautious positioning by investors amid volatile market conditions.

Observations and Future Signals

While USDT and USDC absorbed most of the fresh capital with their widespread trading options and bank accessibility, they now account for over 80% of the market. Concurrently, Ethena’s USDe gained traction through yield offerings but remains susceptible to market fluctuations. Despite the record inflow, a recent decline in active addresses by 23% and transfer volume by 11% suggests that much of this liquidity may be sideline cash rather than active trade.

In summary, while the headlines present a promising outlook with significant capital inflows, the true measure of success will be the sustainable activity and liquidity within the market in the face of potential disruptions.