Saylor’s Bitcoin Strategy

Michael Saylor aims to revolutionize corporate treasury management.

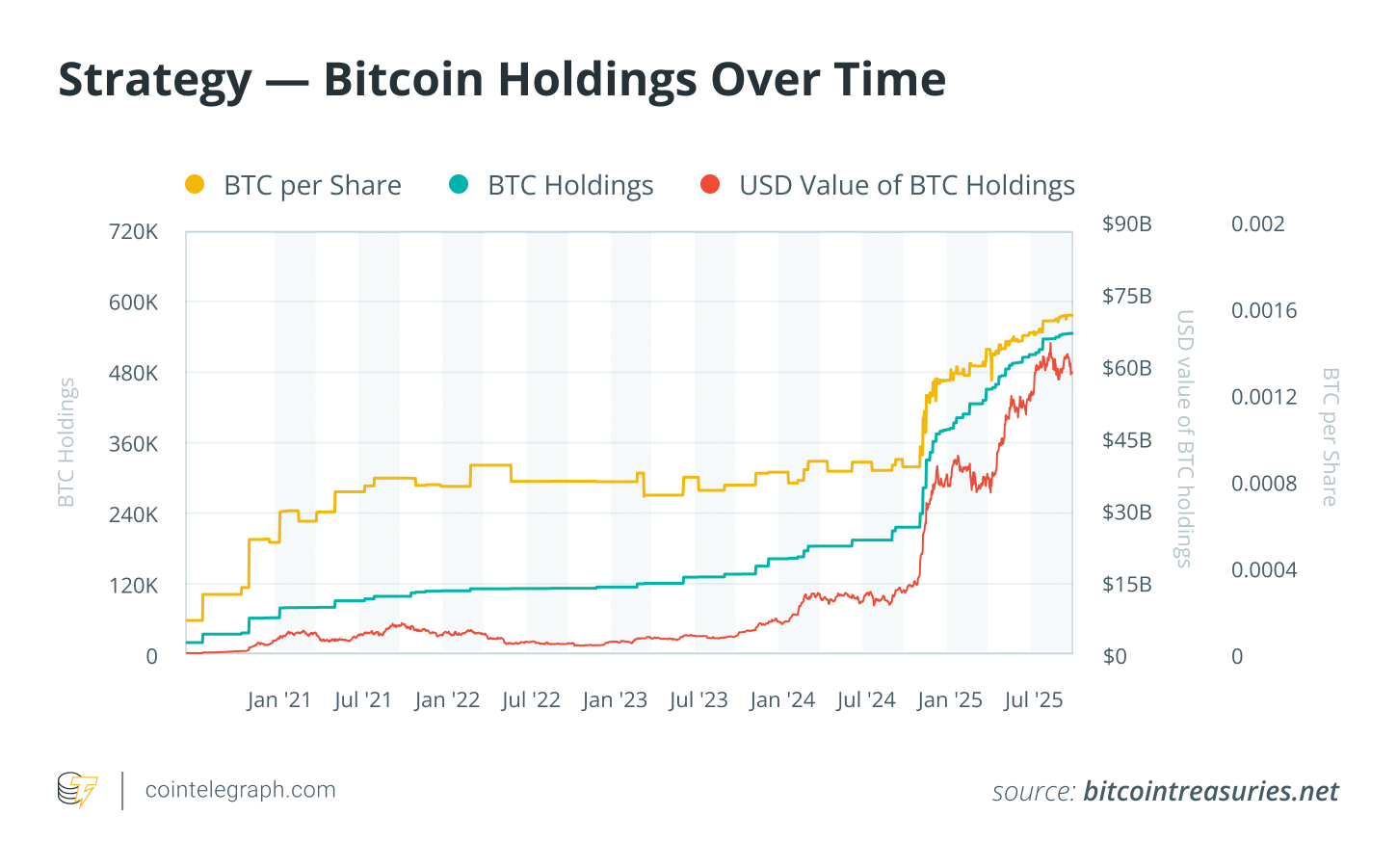

Since August 2020, Saylor’s company, previously known as MicroStrategy and now named Strategy, has emerged as one of the largest public holders of Bitcoin (BTC).

As of September 2025, Strategy reportedly acquired 640,031 BTC worth over $73 billion. The average cost per Bitcoin is in the tens of thousands, indicating significant unrealized profits at current market rates.

For Saylor, Bitcoin serves as both a safeguard against inflation and a reserve asset beyond debasement — positioning the firm for future institutional inflows.

His compelling argument is: if Wall Street channels even 10% of its assets into Bitcoin, the price could surge towards $1 million.

Bitcoin Strategy

Did you know? MicroStrategy’s inaugural Bitcoin purchase as a corporate treasury asset occurred in August 2020, forking out $250 million for BTC.

Bitcoin: The Optimal Treasury Asset

Saylor’s approach is clear yet unwavering: acquire Bitcoin, retain it indefinitely, and integrate it into the company’s foundation.

Since 2020, Strategy has transformed excess cash, debt, and equity raises into a consistent flow of Bitcoin acquisitions. Currently, the company holds 640,031 BTC, accounting for around 3% of Bitcoin’s total supply at an average cost of approximately $73,983 each.

To secure this position, Strategy has utilized various financing mechanisms, including low- or no-interest convertible notes, preferred shares, and other funding instruments designed to minimize shareholder dilution.

Volatility is regarded not as a risk but as an opportunity — seizing price drops, maintaining long-term holdings, and allowing Bitcoin’s inherent scarcity to play out.

Saylor perceives Bitcoin differently than cash, which he refers to as a “melting ice cube” due to inflation’s constant value erosion. Bitcoin’s restricted supply of 21 million coins is enforced by code and halving events that increasingly limit its issuance.

Unlike gold, Bitcoin avoids storage and verification costs while being digital and global, making it resistant to political manipulation.

Additionally, Saylor considers Bitcoin a diversification asset as its correlation with equities and bonds diminishes, providing protective qualities in inflationary environments or aggressive monetary expansion.

For him, Bitcoin embodies an ideal treasury asset: rare, transportable, durable, and equipped for 2025 and beyond.

Did you know? By mid-2025, nearly 95% of all 21 million Bitcoin will have been mined, leaving just over 1 million until the supply cap is reached.

The Path to $1 Million: Saylor’s Las Vegas Prediction

Saylor’s most ambitious assertion is that Bitcoin could reach $1 million for each coin.

The calculations commence with institutional capital: pension funds, insurers, mutual funds, and asset managers collectively govern more than $100 trillion. If just 10% of this pool (approximately $10 trillion-$12 trillion) flowed into Bitcoin, the resultant price effect would be monumental.

Distributing that demand across the fixed 21 million coins implies a valuation approaching $475,000 per BTC.

However, Saylor postulates that the actual supply is significantly lower. It is estimated that between 2.3 million to 3.7 million BTC are permanently irretrievable, and “ancient” supply (coins untouched for over seven years) along with corporate treasuries account for approximately 24% of the complete supply.

Moreover, over 72% of the circulating Bitcoin is deemed illiquid, held by long-term investors who rarely sell.

These factors leave only a minuscule amount of Bitcoin genuinely accessible on the market.

Re-evaluating based on a liquid supply of 16 million-18 million BTC, the same $10 trillion-$12 trillion investment could drive prices to $555,000-$750,000.

With the eventual growth of institutional assets or allocations exceeding 10%, hitting the million-dollar benchmark appears achievable.

However, Saylor cautions that such a transition will not be instantaneous, as regulatory approvals and risk assessments will slow down institutional allocations.

Projection

Projection

Did you know? One significant case of lost Bitcoin involved 8,000 BTC mistakenly thrown into a landfill in Newport, Wales (the hard drive carrying the private key was discarded).

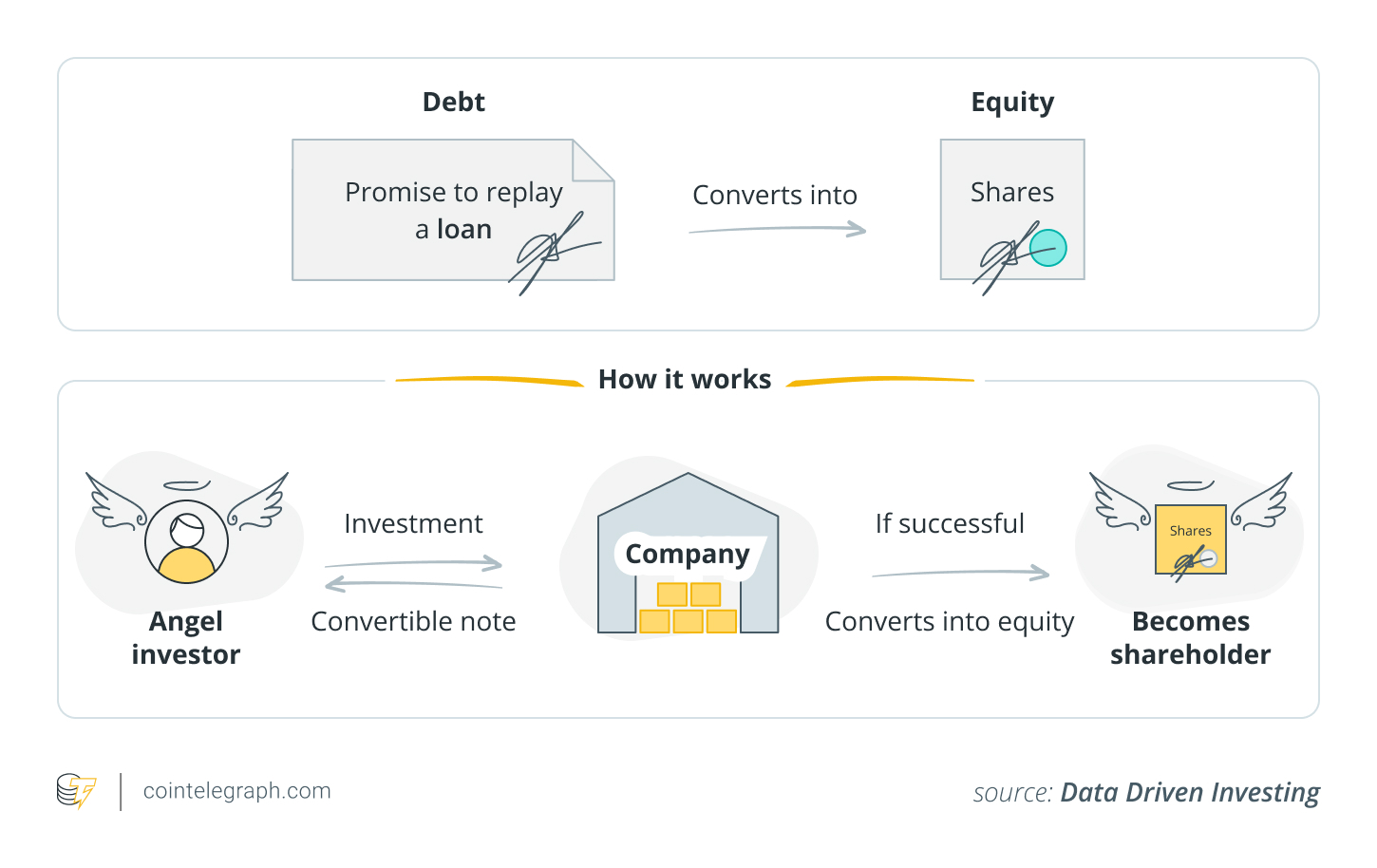

Financing Bitcoin Purchases

Through recent years, Strategy has heavily relied on convertible debt, preferred stock, and innovative equity offerings to finance its Bitcoin purchases.

Convertible Senior Notes

A key aspect of this financing strategy is issuing convertible senior notes, which may convert to equity under specific conditions. These offerings often come with minimal or no interest, minimizing cash outlay.

For instance, in mid-2024, Strategy raised $800 million via a convertible note offering (about $786 million net) at a 35% conversion premium, allowing the purchase of 11,931 BTC at an average price of $65,883.

Preferred Stock and Stretch Offerings

Aside from debt, Strategy has engaged investors through preferred stock offerings. These initiatives often yield higher returns and fewer obligations than traditional debt.

For example, Strategy recently introduced its “Stretch” (STRC) preferred stock with a variable dividend beginning at about 9% per annum, explicitly marketed for Bitcoin acquisitions.

In July 2025, Strategy extended a planned $500-million Stretch issuance to $2 billion due to strong investor interest. Some insiders participated in an offering yielding 11.75%, indicating robust demand for yield-backed investments.

Recent Acquisitions

The most recent public purchase occurred in September 2025, when Strategy acquired 196 BTC at an average cost of $113,048, totaling around $22 million.

Like prior acquisitions, the purchase was funded through common stock sales and preferred stock issuance, rather than from operational cash flow or selling existing Bitcoin.

Funding

Funding

Risks and What Lies Ahead

Strategy’s position as the foremost corporate Bitcoin holder comes with inherent trade-offs.

The organization resembles a leveraged Bitcoin fund, with its stock price mirroring Bitcoin’s price fluctuations. Consequently, as the firm funds new BTC purchases through equity and debt mechanisms, existing shareholders are exposed to potential dilution risks.

Additional risks include:

- Regulatory Risk: Shifts in taxation or accounting regulations could challenge BTC retention.

- Opportunity Cost: Significant capital is immobilized in one volatile asset.

- Institutional Demand Uncertainty: The $1 million projection hinges on Wall Street’s actual allocation of 10%.

Nonetheless, the overarching impact cannot be undervalued. Strategy has facilitated mainstream adoption of Bitcoin in corporate finances and fostered advancements in custody services, exchange-traded funds (ETFs), and institutional over-the-counter markets.

Anticipate the following developments:

- Strategy’s future capital raises and funding mechanisms

- Regulatory clarity concerning Bitcoin accounting and taxation

- Indicators of large asset managers channeling real assets into Bitcoin.

Should these patterns emerge, Saylor’s ambition could fundamentally alter corporate treasury strategies and Bitcoin’s significance in global finance.