The Federal Reserve is considering the proposal of a new type of payment account, intended to increase accessibility for smaller enterprises in the central banking payment ecosystem. This change hints at a resolution to the access issues that have long plagued the cryptocurrency sector.

These proposed accounts aim to offer full access to financial technology firms to engage with the Federal Reserve’s payment services, which have been predominantly available only to larger banks. Governor Christopher J. Waller articulated this vision during his presentation at the Payments Innovation Conference:

“I believe we can and should do more to support those actively transforming the payment system. I have asked Federal Reserve staff to explore the idea of what I am calling a ‘payment account.’”

These types of accounts would be offered to any legitimate institution currently utilizing third-party banks for payment services.

Waller emphasized that the ‘skinny’ master accounts would simplify access to the Fed’s payment systems while managing various risks that the Federal Reserve and the payment system might face.

Federal Reserve Governor Christopher J. Waller at the Payments Innovation Conference.

Federal Reserve Governor Christopher J. Waller speaking at the Payments Innovation Conference. Source: YouTube

Federal Reserve Governor Christopher J. Waller at the Payments Innovation Conference.

Federal Reserve Governor Christopher J. Waller speaking at the Payments Innovation Conference. Source: YouTube

While still in experimentation, this initiative reflects a significant movement towards integrating fintech and crypto payment firms within traditional finance structures. Industry analysts consider this a favorable progress for the cryptocurrency world, which has encountered significant banking access issues.

During the administration of former President Joe Biden, numerous tech and crypto leaders faced banking restrictions, a situation many have termed “Operation Chokepoint 2.0.”

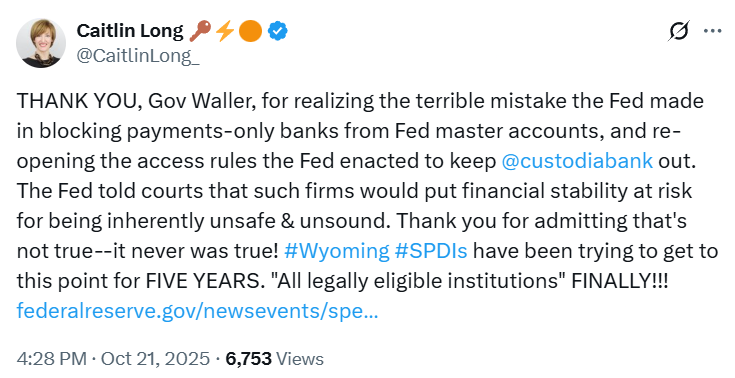

Caitlin Long’s X post about access rules.

Source: Caitlin Long

Caitlin Long’s X post about access rules.

Source: Caitlin Long

“THANK YOU, Gov Waller, for recognizing the severe error the Fed made in blocking access to master accounts for payments-only banks and for revisiting the Fed’s restrictive policies that prevented @custodiabank from participation.”

Long remarked on X, further adding:

“The Fed argued that such firms posed risks to financial stability. Thank you for acknowledging that this was a falsehood—it never held true!”

The recent collapses of banks favoring crypto in 2023 intensified the allegations of Operation Chokepoint 2.0. Critics argue that there is an orchestrated effort to pressure banks into severing ties with cryptocurrency operations.

Fed Engages with Advanced Payment Technologies

The Federal Reserve has been looking into blockchain technology for payment solutions in conjunction with the idea of ‘skinny’ master accounts.

Waller mentioned that the Fed is studying blockchain and AI for payment applications:

“We are also looking ahead, conducting hands-on research on tokenization, smart contracts, and the intersection of AI and payments for our payment systems.”

“Our goal is to comprehend the innovations occurring in the payment landscape and to assess if these technologies can yield opportunities to enhance our own payment infrastructure.”

Related read: Magazine: Bitcoin OG Willy Woo has sold most of his Bitcoin — Here’s why

Tags:

- #Bitcoin

- #Blockchain

- #Cryptocurrencies

- #Altcoin

- #FederalReserve

- #Law

- #Business

- #Government

- #Banking

- #CentralBank

- #Payments

- #Adoption

- #USGovernment

- #AI

- #Micropayments

- #BankAccounts

- #Tokens

- #Stablecoin

- #Web3

- #Regulation