Understanding the process of filing your crypto taxes is vital for your investment or trading journey. Here’s a guide that covers everything you need to know for 2025.

Key Points to Remember:

- Tax Obligation: Crypto is taxed as property; taxes are incurred on sales, exchanges, and earnings, but not for simply holding crypto.

- Tax Events: Taxable activities include trading, mining, staking, and airdrops, while transactions between your wallets usually aren’t taxable.

- Regulatory Differences: The IRS treats crypto as a digital asset, the HMRC applies distinct capital and income taxes, while EU member states have varying frameworks under the MiCA regulation.

- Tax Software: Utilize software like Koinly or CoinLedger to simplify reporting and save time.

Understanding Crypto Taxation

Overview:

- Taxable Events: Crypto taxes apply only when you sell or trade your assets; simply holding does not incur a tax burden.

- Types of Taxes: Income tax applies to staking and mining, whereas capital gains tax applies to profits from trading.

A detailed approach to filing crypto taxes involves determining which transactions are taxable and adhering to your local tax authority’s guidelines.

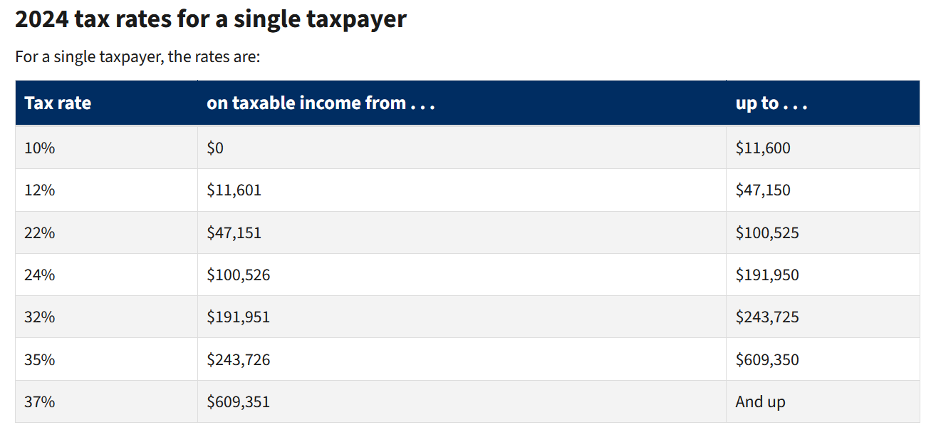

Crypto Taxation in the US

- The IRS requires annual reporting of all crypto transactions. Tax year runs from January to December, with an April 15 deadline.

Crypto Taxation in the UK

- HMRC applies income and capital gains taxes and has set specific filing deadlines.

Crypto Taxation in the EU

- Countries adhere to their regulations but generally follow EU guidelines on crypto taxation.

Recommended Software Tools

Using efficient tools can streamline your tax reporting process significantly. Here are some reliable options:

- Koinly: Comprehensive and user-friendly.

- CoinLedger: Ideal for busy traders with features supporting various asset types.

Steps to File Your Crypto Taxes

- Choose Software: Select suitable tax software for your needs.

- Create Account: Set up your account with specific details.

- Link Accounts: Connect your exchanges and wallets.

- Review Transactions: Ensure all your transactions are accurately reported.

- Generate Report: Produce and file your tax report accordingly.

Common Pitfalls to Avoid

- Ensure you report all transactions, not just those from central exchanges.

- Avoid misclassifying non-taxable events and do consider transaction fees.

What’s New for 2025-2026

Be on the lookout for new forms such as the Form 1099-DA, which will report gross proceeds from digital asset sales starting January 2025. Additionally, broker-reporting requirements in DeFi have been repealed.

Crypto taxation has become stricter, where compliance is crucial to avoid audits and potential fines. Understanding these aspects thoroughly will not only save money but also time.